Subnet 67 Crash: What Happened in Tenex?

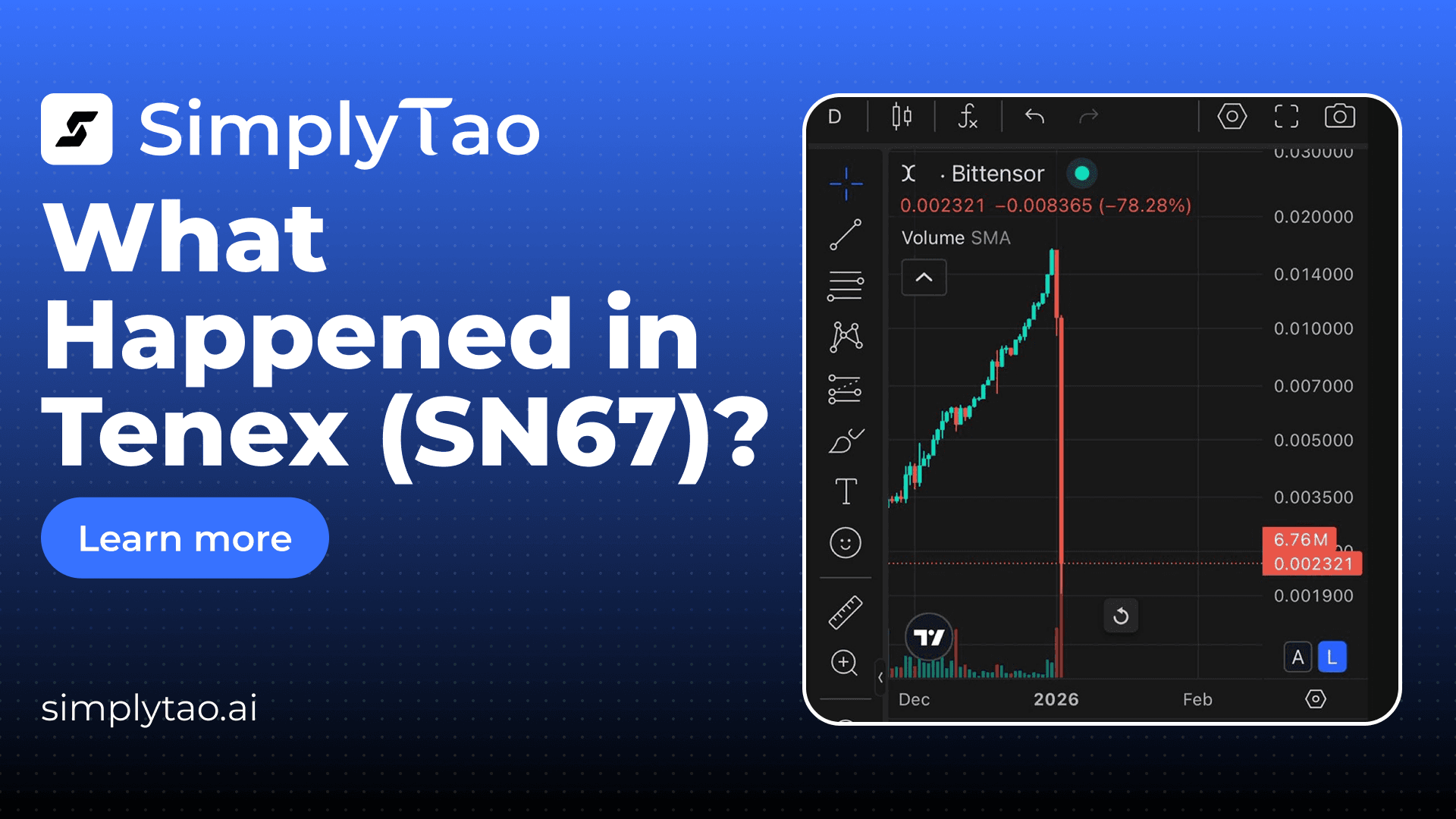

A recent incident in the Bittensor ecosystem drew attention after the Tenex subnet (SN67) suffered an exploit that drained liquidity and effectively collapsed the subnet’s token economy. Subnet 67 operated as a liquidity subnet, where participants deposited assets to provide liquidity and, in return, earned high APY rewards. It was widely framed as a relatively safe way to earn elevated yield. That perception proved incorrect when a smart contract vulnerability was exploited, emptying the liquidity pool and triggering a rapid price decline.

🚨The key point: this event did not compromise Bittensor’s base protocol. The failure was tied to subnet-level code and operational design, not to Bittensor as the underlying platform. Investors who deposited tokens into the Tenex liquidity system or staked within Subnet 67 appear to face losses that are largely irrecoverable, at least based on the publicly discussed information in the incident analysis.

The Exploit and the Tenex Collapse

Tenex’s core mechanism depended on an EVM-based smart contract that managed liquidity and payouts. The exploit drained the liquidity pool, which removed the primary support for price stability and market confidence. Once liquidity vanished, the token price fell sharply – an outcome that is structurally common in liquidity-driven systems where pool solvency is the foundation of both redemption value and price discovery.

The attacker’s identity remains unspecified in the available analysis. That uncertainty matters because it keeps multiple risk models on the table, from an external exploit to potential insider involvement. Regardless of who executed the exploit, the effect was the same: liquidity providers and subnet participants bore the downside when the system’s critical contract path failed.

Why This Was Not “Bittensor Getting Hacked”

It is important to separate platform risk from subnet risk. The incident analysis emphasizes that Bittensor itself was not hacked – rather, Subnet 67 was an example of how subnet owners can deploy logic that introduces new attack surfaces. Bittensor’s architecture allows subnets to implement their own mechanisms and contracts, which expands innovation potential but also permits unsafe or insufficiently hardened designs to exist inside the broader ecosystem.

Bittensor does impose frictions – such as the cost and requirements associated with creating a subnet and expectations around open-source components – which helps reduce low-effort scams. However, that friction does not eliminate the possibility of exploitable smart contracts, fragile tokenomics, or incentive structures that attract capital faster than the system can safely sustain.

A Tenex Token Price That Outpaced Trust

Subnet 67’s token price reportedly rose to around 0.015 TOW, roughly three times higher than the median subnet prices mentioned in the analysis. Price can rise for many reasons but the key issue is whether price is supported by credible fundamentals: proven utility, reputable builders, transparent governance, and robust security.

In this case, the combination of high valuation, anonymous operators, and extreme concentration risk should have been interpreted as a convergence of red flags. High price is not itself a problem, but high price without justified trust increases the probability that the market is being driven by incentives rather than resilient value creation.

Practical Due Diligence Lessons for Subnet Investors

This incident reinforces a disciplined approach to evaluating Bittensor subnets as investable opportunities. First, investors should treat token concentration as a first-class risk measure: a largest-holder share above 50% is not a minor concern – it is a structural instability. Second, investors should strongly prefer subnets with transparent teams, clear operations, and reputational stakes that align incentives over time. Third, investors should assume that any system involving smart contracts introduces additional attack surface, and they should scrutinize not only whether an audit exists, but what it actually covered, how the system is administered, and whether privileged actions are constrained by strong controls.

Finally, investors should avoid concentrating exposure. A subnet can look compelling until a single failure mode materializes. Diversification across multiple subnets, combined with conservative position sizing in higher-risk designs, is not just a portfolio preference – it is a survival mechanism in adversarial environments.

Source: TAO Templar video